All Categories

Featured

Table of Contents

The are entire life insurance policy and global life insurance policy. The cash money value is not added to the fatality advantage.

After 10 years, the money value has grown to around $150,000. He secures a tax-free car loan of $50,000 to begin a service with his sibling. The policy lending rates of interest is 6%. He settles the finance over the next 5 years. Going this route, the rate of interest he pays goes back into his policy's money value as opposed to an economic institution.

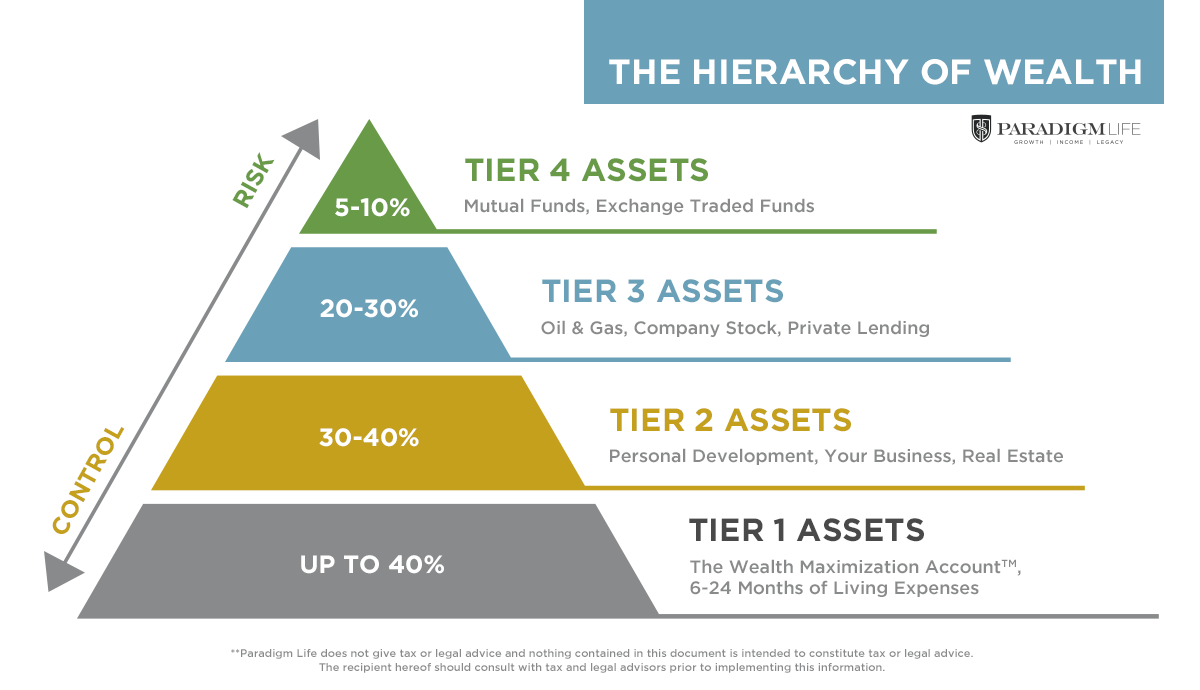

Create Your Own Banking System

The idea of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a finance professional and fan of the Austrian school of business economics, which advocates that the value of products aren't explicitly the outcome of standard economic structures like supply and demand. Rather, people value cash and goods differently based on their economic condition and requirements.

Among the challenges of standard financial, according to Nash, was high-interest prices on lendings. As well several individuals, himself included, entered into monetary difficulty as a result of reliance on banking organizations. Long as banks set the rate of interest rates and funding terms, people really did not have control over their own wide range. Becoming your own lender, Nash established, would certainly place you in control over your monetary future.

Infinite Financial requires you to have your financial future. For goal-oriented people, it can be the finest monetary device ever before. Below are the benefits of Infinite Banking: Probably the solitary most advantageous element of Infinite Financial is that it improves your cash money circulation.

Dividend-paying entire life insurance is very reduced danger and uses you, the insurance policy holder, a large amount of control. The control that Infinite Banking offers can best be grouped into two classifications: tax advantages and possession securities - priority banking visa infinite credit card. One of the reasons entire life insurance policy is ideal for Infinite Banking is how it's taxed.

Infinite Banking Concept Pros And Cons

When you make use of whole life insurance for Infinite Financial, you get in into a personal agreement between you and your insurance provider. This personal privacy supplies specific property securities not located in other economic vehicles. These protections might vary from state to state, they can include protection from property searches and seizures, defense from reasonings and defense from lenders.

Entire life insurance plans are non-correlated possessions. This is why they function so well as the monetary structure of Infinite Banking. No matter of what occurs in the market (stock, real estate, or otherwise), your insurance policy retains its worth.

Market-based financial investments grow wide range much faster yet are exposed to market changes, making them naturally dangerous. What if there were a 3rd container that supplied security but also modest, guaranteed returns? Entire life insurance policy is that 3rd pail. Not just is the price of return on your whole life insurance policy policy assured, your survivor benefit and costs are additionally ensured.

Below are its main benefits: Liquidity and accessibility: Policy finances provide instant accessibility to funds without the limitations of traditional bank lendings. Tax obligation efficiency: The cash money value expands tax-deferred, and policy car loans are tax-free, making it a tax-efficient device for constructing riches.

Infinite Banking Concept

Asset protection: In many states, the money worth of life insurance policy is protected from lenders, adding an additional layer of financial protection. While Infinite Financial has its qualities, it isn't a one-size-fits-all option, and it comes with substantial disadvantages. Right here's why it may not be the most effective strategy: Infinite Banking usually calls for complex plan structuring, which can puzzle insurance policy holders.

Envision never having to worry regarding bank loans or high rate of interest prices again. That's the power of infinite financial life insurance.

There's no collection car loan term, and you have the flexibility to pick the settlement routine, which can be as leisurely as repaying the car loan at the time of fatality. This flexibility reaches the maintenance of the loans, where you can go with interest-only settlements, keeping the finance equilibrium flat and convenient.

Holding money in an IUL repaired account being credited rate of interest can usually be much better than holding the money on deposit at a bank.: You've always desired for opening your own bakery. You can borrow from your IUL plan to cover the initial costs of leasing an area, buying devices, and employing staff.

Does Infinite Banking Work

Individual loans can be gotten from conventional financial institutions and credit scores unions. Borrowing cash on a credit rating card is typically extremely expensive with yearly percentage prices of passion (APR) commonly reaching 20% to 30% or even more a year.

The tax obligation therapy of policy financings can vary substantially depending on your nation of residence and the particular regards to your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan financings are usually tax-free, using a considerable advantage. In other territories, there may be tax effects to consider, such as potential tax obligations on the car loan.

Term life insurance policy just offers a survivor benefit, with no money value accumulation. This indicates there's no money worth to obtain versus. This article is authored by Carlton Crabbe, Ceo of Capital permanently, a professional in supplying indexed global life insurance accounts. The details offered in this short article is for educational and informative purposes only and should not be interpreted as economic or financial investment advice.

For financing police officers, the extensive guidelines enforced by the CFPB can be seen as difficult and restrictive. Funding officers typically say that the CFPB's guidelines produce unneeded red tape, leading to even more paperwork and slower financing handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) demands, while targeted at safeguarding consumers, can lead to hold-ups in shutting bargains and enhanced functional prices.

{kind=link}

Latest Posts

Be Your Own Bank

Becoming Your Own Bank

Be Your Own Bank: Practical Tips